Insights & Commentary

Investment Letter – February 2026

Profits, Power Projection and Portfolio Discipline

Welcome to our February Investment Letter.

In this edition, we outline the key takeaways from the latest earnings results reported by companies in Australia and the United States. We also provide our perspective on the unfolding US–Israel conflict with Iran and its broader implications for markets.

PORTFOLIO COMMENTARY

February was a busy reporting month. In Australia, companies reported their half- or full-year results to 31 December 2025, while in the US most companies reported quarterly earnings.

AUSTRALIAN REPORTING SEASON FEBRUARY 2026 – MOSTLY POSITIVE

The Australian share market rose over +3% in February, including the sharp Monday morning response this week to the renewed Iran conflict over the weekend.

The market continues to trade near record highs, but it has not been a rising tide lifting all boats. Companies that beat expectations and upgraded guidance were rewarded handsomely. Several holdings in our portfolios, including Telstra, Pexa, Amcor and Sonic Healthcare, posted strong returns following their results, while those that disappointed were sold off just as quickly. CSL has been the main laggard for us.

Overall, however, the majority of companies exceeded expectations.

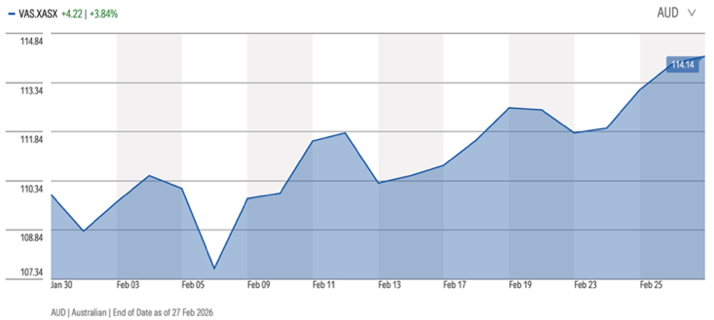

Figure 1: Australian Shares (VAS ETF) Performance over February 2026 was +3.8%

Source: Morningstar as at 02 March 2026

Source: Morningstar as at 02 March 2026

Sector leadership was driven by Materials (+8%) and Financials/Banks (+10%), led by strong results from BHP and CBA. Dividend growth from both businesses was also notable, signalling that management teams are comfortable sharing surplus profits and remain confident in near-term earnings conditions, rather than retaining excess cash.

Real estate stocks were a modest drag over the month, not due to weak results (which were generally positive), but because sentiment softened following an RBA rate increase to 3.85%, with markets anticipating another move higher toward ~4.1% in coming months

Healthcare delivered mixed outcomes. Sonic Healthcare (with exposure to GP clinics and diagnostics) rose +4%, while CSL fell -19%. This divergence reflects execution and expectations rather than profitability: the market had underestimated Sonic’s strong profit momentum and stable guidance, while CSL faced heightened competitive pressures in plasma and some near-term demand softness, falling short of the market’s growth expectations. CSL has also entered a leadership transition, with a new CEO search underway. We continue to hold CSL as a long-term position; it remains a global-scale business with a strong competitive position in plasma, though it may take time to rebuild momentum.

Telstra, a stock that features prominently across our portfolios, delivered a strong First Half (1H26) result. Profit rose around +9% and exceeded market expectations, supported by continued momentum in the mobile division. The interim dividend increased +10.5% (from 9.5cps to 10.5cps), alongside an expanded on-market buyback, reinforcing Telstra’s role as a high-quality defensive compounder with disciplined capital management.

We view Telstra as a “picks and shovels” exposure to Australia’s digital economy: it owns and operates critical communications infrastructure and runs the country’s leading mobile network, positioning it to benefit as data consumption continues to rise. Consistent with this theme, Telstra’s results presentation shows mobile service revenue up +5.6% and Average Revenue Per User (ARPU) up +5.1%, reflecting both customer growth and pricing traction.

Interestingly, JB Hi-Fi also noted that customers are prioritising spending on technology, particularly smartphones and related devices, highlighting that connectivity and devices are becoming less discretionary as AI features become mainstream.

Technology stocks were another sector, like healthcare, with highly divergent results and share-price reactions. We have limited exposure to Australian technology, largely because valuations have often been stretched relative to fundamentals. That view has been partly vindicated: bellwether names such as WiseTech and Xero, both industry-leading businesses, saw sharp share-price declines amid growing concern about AI-driven disruption and their limited regulatory protection.

One Australian technology holding we do maintain is PEXA Group, which benefits from a very different type of advantage. PEXA’s moat is regulatory and structural, it operates on mandated digital conveyancing “rails” with high barriers to entry, whereas WiseTech and Xero rely on commercial moats (product leadership, integration ecosystems and switching costs) that are more directly exposed to technological disruption and competitive feature replication. PEXA also continues to show solid operational momentum. Over the month, PEXA rose +12%, compared with WiseTech down -21% and Xero down -15%.

In summary, overall, February reinforced that Australian equities remain well supported with positive revenue and profit momentum and nice dividend growth surprises, but the market is increasingly selective, rewarding strong execution and credible guidance while punishing disappointments. The overall outlook remains constructive for Australian equities. Analyst consensus is currently forecasting +10% to +12% EPS (profit) growth for FY26, followed by approximately +10% growth in FY27 (subject to revision as conditions evolve).

US REPORTING SEASON FEBRUARY 2026

In the US, the Q4 2025 reporting season was strong overall.

Despite this, US equities were modestly lower in February, driven by three main factors: (1) renewed concerns that large technology companies may be overspending on AI (a view we do not fully share), (2) a rotation within parts of the technology sector, particularly software, where companies such as SAP, Salesforce and Adobe came under pressure on fears that AI could disrupt elements of their business models, and (3) a weaker US dollar, which detracted from Australian-dollar returns on global equities.

Figure 2: Global stocks (QHAL ETF) lagged Australian shares (VAS ETF)

Source: Morningstar as at 02 March 2026

Source: Morningstar as at 02 March 2026

Before turning to the detail of the reporting season, it is worth noting a paradox in current market thinking. On the one hand, the market is worried that AI spending is excessive, implying the commercial use case may be less powerful than advertised. On the other, it has simultaneously sold down major global software companies on the view that AI will materially disrupt their business models, implying AI is commercially powerful and adoption will be rapid.

Both arguments cannot be true at the same time in the same magnitude; the reality is likely to sit somewhere in between, with winners and losers emerging over time.

Turning to the reporting season itself, almost all S&P 500 companies have now reported, and US corporates delivered profit growth of +14.2%, well ahead of expectations of +8%. This marked the fifth consecutive quarter of double-digit earnings growth.

Revenue was also up an impressive +9%, extending the US market’s long run of topline growth to a 21st consecutive quarter. Overall, most companies beat expectations.

By sector, technology and industrials were the standout performers. Technology delivered earnings growth of 33% and revenue growth of 22%, with net margins expanding to 29.0% (up from 26.8% a year earlier and well above the sector’s five-year average). The gains were broad-based across the AI supply chain, from NVIDIA’s continued semiconductor dominance and Microsoft’s cloud expansion to Apple’s revenue beat of US$143.8 billion versus expectations of US$138.4 billion.

Industrials told a similarly compelling story on the fundamentals that matter most. Revenue grew +8% and net margins expanded to 12.5% from 10.7%, again ahead of the five-year average of 9.3%. Caterpillar—a bellwether with exposure across construction, oil & gas, infrastructure, power generation and data centres—posted record Q4 sales of US$19.1 billion on strong demand for construction and power equipment, while GE Vernova benefited directly from the acceleration in data-centre build-out.

In short, both technology and industrials were supported by insatiable demand for AI, lifting the companies and industries that make up the broader “AI industrial complex”.

In healthcare, the US Q4 reporting season delivered a steady set of fundamentals: sector earnings growth was broadly flat (+0.4% y/y), but revenue growth was strong (+10.4% y/y), highlighting resilient underlying demand even as margins were mixed across sub-sectors.

Looking ahead, analyst expectations point to a re-acceleration in profit growth, with S&P 500 healthcare earnings forecast to grow +6.8% in 2026 and +11.4% in 2027. We believe this improving earnings outlook, combined with the sector’s defensive characteristics and the potential for valuation catch-up after several years in which technology and industrials dominated performance, positions healthcare to deliver attractive growth over the coming years.

For our exposure via the VanEck Health ETF (HLTH), this remains a constructive backdrop, providing diversified access to global healthcare leaders with meaningful exposure to large US names.

Figure 3: Five-year performance of the technology- and industrials-anchored Global Quality Stocks ETF (QHAL) versus the Global Healthcare Stocks ETF (HLTH)

Source: Morningstar as at 02 March 2026

Source: Morningstar as at 02 March 2026

In summary, the US earnings season reinforced that market leadership remains concentrated in AI-linked parts of the economy, particularly technology and industrials, while healthcare is quietly rebuilding momentum. With a supportive earnings outlook and defensive qualities, healthcare has the potential to contribute more meaningfully to returns as sector leadership broadens beyond the recent winners.

MARKET OUTLOOK

As we were preparing to publish this letter, hostilities between the United States/Israel and Iran resumed, less than twelve months after the brief 12-day conflict/war of June 2025.

Our role is to minimise speculating on political motives, but to assess structural consequences.

Following the 2025 conflict, U.S. officials stated that Iran’s nuclear capabilities had been materially degraded. Independent analysts have publicly noted that they have not seen clear evidence of Iran reconstituting an active nuclear weapons program. At the time of writing, no publicly released intelligence has demonstrated an imminent nuclear threat.

Yet, here we are with another war with Iran based on rhetoric rather than evidence of Iran being an imminent nuclear threat.

The renewed action appears to have been undertaken under existing US presidential executive authority rather than through a multilateral framework via the Congress or the UN Security Council.

Rather than focus on and contest the political narratives, we consider what this signals about the broader global system.

A STRUCTURAL SHIFT IN THE GLOBAL ORDER

The defining feature of this episode is not the specific actors involved, but the continued movement away from broad multilateral consensus toward more direct power projection.

This trend has been building for several years, across Eastern Europe (Russia’s aggression in Ukraine), the Middle East, and Asia (China’s assertiveness toward Taiwan).

What we are observing is a world in which geopolitical risk is no longer episodic, but structural.

That distinction matters for investors.

Structural geopolitical risk does not dissipate quickly. It influences energy markets, defence spending, trade routes, shipping costs, and currency dynamics. It also affects central bank behaviour. In recent years, we have seen a gradual shift in foreign exchange reserve management, with gold increasingly taking the place of U.S. dollar reserves among countries that are not closely aligned with the United States, China being a prominent example.

This structural move toward direct power projection changes how nations think about economic security. When physical security risks rise, economic policy becomes more defensive and strategic.

Political alliances are also becoming more fluid. Long-standing arrangements are under strain from overt displays of national interest. For example, U.S. commentary regarding Greenland - a territory under Danish sovereignty and therefore within the NATO alliance framework - illustrates how traditional alliance norms are being tested. This fluidity is contributing to greater mistrust between nations and the emergence of more transactional, multipolar relationships.

That mistrust has already been reflected in capital flows. Emerging market central banks have been accumulating gold as a neutral reserve asset. More recently, the latest escalation involving Iran appears to have extended that mistrust to investors. In prior conflict episodes, capital typically flowed into U.S. Treasuries as the primary safe haven. This time, however, as markets reopened following the outbreak of the latest Iran war, gold strengthened by +2% while U.S. Treasuries weakened by a similar magnitude.

The signal is subtle but important: safe-haven behaviour may be evolving alongside the broader structural shift in the global order.

Turning to Iran.

INCENTIVES AND DETERRENCE – WHY HAS IRAN PURSUED A NUCLEAR CAPABILITY?

Iran’s long-term strategic posture has been shaped in part by its eight-year war with Iraq in the 1980s, during which chemical weapons were used with limited international consequence for Iraq. Strategic thinkers in Tehran have long argued that vulnerability invites aggression, and that durable deterrence, potentially including a nuclear capability, is essential to regime security.

Whether one agrees with that doctrine or not, the internal logic is clear: states that perceive themselves as vulnerable in a world increasingly defined by direct power projection seek stronger forms of protection. In some cases, that includes the pursuit or preservation of nuclear capability.

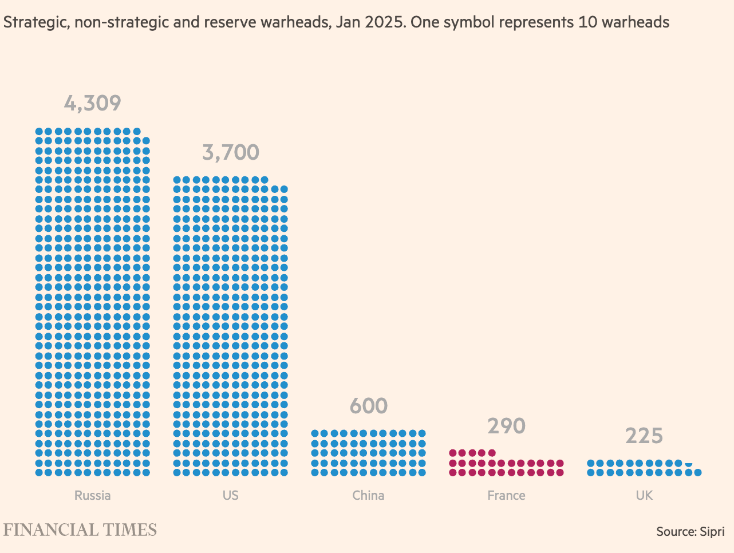

Recent developments in Europe illustrate how the logic of deterrence extends beyond Iran. France, a recognised nuclear power, has indicated a willingness to strengthen its bordering countries’ sovereignty by offering France’s nuclear deterrence umbrella, amid concerns about Russia’s aggression in Europe. This reflects a broader reassessment of security guarantees across the continent.

Such shifts raise important strategic questions. If nuclear deterrence is increasingly seen as shareable or expandable within alliances, how might other powers respond?

Russia, for example, possesses a far larger nuclear arsenal than France. One could imagine a scenario in which Moscow sought to extend its nuclear umbrella to its partners, including Iran, as a counterweight to Western security consolidation.

Figure 4: France's nuclear warhead stockpile is dwarfed by that of Russia and the US

That said, any direct transfer or deployment of nuclear weapons to third countries would represent an unprecedented escalation, with profound global consequences. Major powers, including the United States, would face significant strategic decisions in such a scenario.

The broader point for investors is to recognise that deterrence dynamics are becoming more central to global geopolitics. As nuclear postures evolve, so too does the risk architecture underpinning markets

THE DIRECT & MORE IMMEDIATE IMPACT OF US-ISRAEL AND IRAN WAR IN 2026

The most immediate concern for investors is the potential blocking of the Strait of Hormuz by Iran, or, if not a complete blockade, a disruption to the flow of oil and gas from the region to global markets. Iran has repeatedly threatened such actions, but it does not hold legal sovereignty over the Strait (not that compliance to the international law is high on any country’s agenda right now), indeed, no country does.

The waterway constitutes international waters under customary maritime law, with freedom of navigation guaranteed to both commercial and naval vessels. This shared international status means that any unilateral attempt to prevent transit would be viewed as a serious violation of international norms and would likely provoke a forceful response.

Figure 5: Strait of Hormuz

Source: Google

Source: Google

Any sustained disruption to the Strait would almost certainly result in materially higher oil and LNG prices. So far this week, oil and gas prices have risen by approximately +7%, meaningful, but modest relative to the spikes observed during comparable historical crises. Global equity markets have also declined only moderately. This suggests that markets are currently pricing a relatively swift resolution rather than a prolonged conflict. Time will tell.

Given that this war appears preventative in nature rather than a response to an imminent threat, and was initiated by the United States, it could also be halted suddenly by the United States. With President Trump in a midterm election year, it is unlikely he would sustain an extended bombing campaign if markets were to react sharply and energy disruptions began feeding materially into inflation and higher interest rates in the U.S. and other advanced economies.

Approximately 20% of global oil supply and a similar share of LNG trade transit this narrow waterway, with the majority destined for energy-importing Asian economies such as China, Japan, South Korea, and India. In a scenario involving prolonged conflict and interrupted supply, inflationary pressures would be transmitted disproportionately to these nations.

The United States, now a net energy exporter, faces less direct supply vulnerability and could initially benefit from higher prices and increased demand for substitute supply. However, inflation would still feed back into the U.S. through higher import costs from trading partners such as China and other manufacturing economies.

A prolonged interruption would quickly transmit through global energy benchmarks, lifting fuel costs, raising headline inflation, and pressuring real household incomes worldwide. Markets would likely reprice inflation expectations rapidly, increasing volatility across bonds, currencies, and equity markets.

That said, a complete and sustained closure of the Strait remains a high-risk strategy for Iran — not least because its own exports also move through the same passage. It is also a scenario that U.S. military planners have long war-gamed. The U.S. Fifth Fleet is permanently positioned in the region to deter and respond to threats to freedom of navigation, and contingency planning has consistently incorporated scenarios involving disrupted Hormuz traffic.

Historical precedent from the 1980s “Tanker War” between Iran and Iraq demonstrates that even amid sustained attacks on shipping, coordinated naval escorts, mine-clearing operations, and targeted counter-measures were ultimately successful in keeping oil flowing.

While any disruption would likely drive prices higher initially, the probability that the United States and its allies would deploy carrier strike groups, convoy protection, and mine countermeasure operations to reopen and secure transit is high.

The key investment risk, therefore, is not necessarily a permanent shutdown of supply, but the magnitude and duration of the price shock and inflation impulse before stabilisation efforts take effect.

Periods of heightened volatility may, in time, present opportunities to deploy capital at attractive valuations. In the meantime, we remain prudent and patient in our positioning. Portfolios are currently underweight to neutral in growth assets, maintain sufficient liquidity buffers, and remain adequately diversified to navigate elevated market volatility.

LONGER TERM FINANCIAL AND RESERVE IMPLICATIONS

A more fragmented geopolitical environment encourages diversification.

We are not witnessing an abrupt abandonment of the U.S. dollar system. The dollar remains dominant in global trade settlement, foreign exchange reserves, and capital markets.

However, we are observing incremental diversification of reserves among several non-aligned and emerging economies in this environment of heightened direct power projection.

Gold remains relevant in this context, as discussed earlier. It functions as a neutral reserve asset outside any sovereign liability structure. Continued central bank accumulation in recent years reflects a broader desire for resilience within reserve frameworks. This is not ideological positioning; it is sovereign-level risk management.

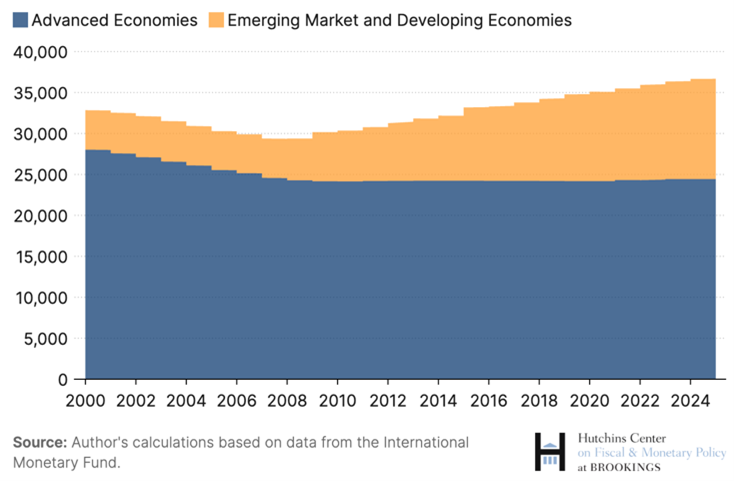

The chart below shows that emerging market economies such as China and India (highlighted in orange) have been steadily increasing their share of gold holdings, with the trend continuing into 2025.

Figure 6: Global central bank gold holdings, 2000-2024 (Tons)

The natural question is: how much further could this diversification go?

The following table provides perspective.

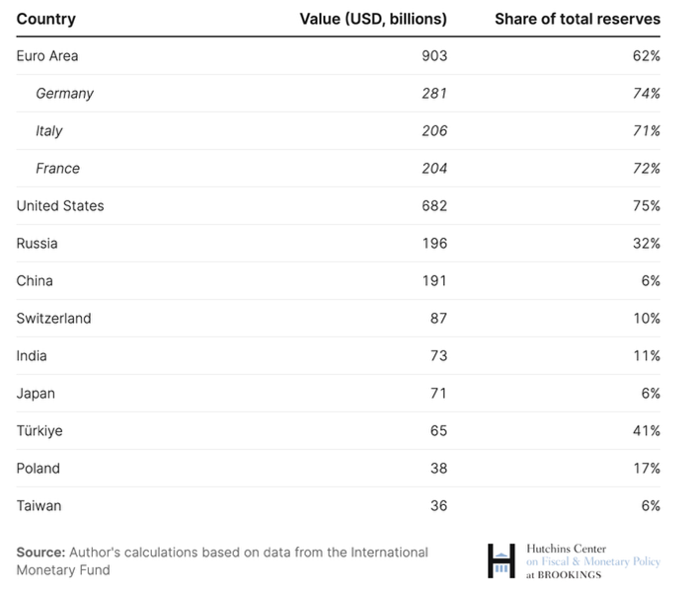

Figure 7: Monetary gold holdings by central banks, 2024

While advanced economies such as Germany and France hold approximately 60–70% of their reserves in gold, China and India hold only around 6–11%.

In other words, emerging economies remain materially underweight gold relative to advanced nations. Should they choose to converge even partially toward developed-market reserve structures, there remains substantial scope for additional gold accumulation.

From a sovereign perspective, increasing allocations to gold can be viewed as an effort to enhance perceived safety and autonomy within reserve portfolios - holding value in an asset that is politically neutral and not directly linked to another nation’s economics or politics.

PORTFOLIO DISCIPLINE IN A FRAGMENTED WORLD

At Sovereign Advisors, our response to geopolitical escalation is discipline rather than reaction.

We:

- Maintain diversified exposures across regions and asset classes.

- Actively manage currency risk.

- Hold neutral reserve assets within prudent ranges.

- Avoid excessive concentration in any single geopolitical outcome.

- Use periods of volatility selectively to add to high-quality growth exposures at attractive valuations.

Geopolitical events are rarely forecastable with precision. Structural positioning, however, is within our control. In a world where geopolitical volatility appears persistent rather than temporary, resilience becomes a core investment advantage.

Our focus remains unchanged: preserve balance, manage risk thoughtfully, and compound capital prudently over time

Book Review – Iran’s Grand Strategy – A Political History (2025)

Author: Vali Nasr

Publisher: Princeton University Press

Author: Vali Nasr

Publisher: Princeton University Press

As the United States and Iran once again exchange direct strikes in 2026, investors are understandably asking: Is this ideological escalation, or strategic design?

Vali Nasr’s Iran’s Grand Strategy provides a timely and sobering answer. It argues that Iran’s behaviour is not impulsive revolutionary zeal, nor theological fatalism. Rather, it reflects a coherent, historically rooted grand strategy developed over four decades.

The Core Argument

Nasr contends that Iran has evolved beyond its revolutionary origins into what is effectively a hard-edged nation-state pursuing security, deterrence, and regional primacy.

The book traces how:

- The trauma of the Iran-Iraq War (1980–1988) forged a doctrine of “sacred defence.”

- The experience of isolation and sanctions reinforced a commitment to self-reliance and asymmetry.

- The U.S. invasions of Afghanistan and Iraq validated Iran’s suspicion of encirclement.

- The “Axis of Resistance” became Iran’s forward-defence architecture.

Iran’s strategy is not to defeat the United States militarily. It is to exhaust it.

Nasr recounts a revealing exchange between an Iranian official and Henry Kissinger: Iran’s goal, the official explained, is not ideological conquest but strategic patience, outlasting American will in the region.

Where many interpretations of Nasr’s thesis may seem challenged by the events of 2026 is on the assumption that Iran would avoid direct interstate war and especially large-scale attacks on its territory. The U.S. and allied strikes of 28 February have clearly signalled broader ambitions, including an explicit aim to degrade Iran’s regime and its leadership, and possibly, as some Western statements suggest, to catalyse regime change.

Nasr’s framework of “strategic patience” remains a useful starting point for understanding Iran’s behaviour, even amid the escalations of 2026.

Where Nasr’s Framework Truly Breaks

The doctrine collapses only if:

- 1. The regime fractures internally (elite split)

- 2. Military command coherence fails

- 3. Economic collapse triggers uncontrollable social unrest

- 4. The US commits to sustained escalation beyond strike-and-withdraw

Short of that, Iran’s system is designed for siege conditions